No Good News On ’20 Gas Prices: EIA

20 January 2020

Anyone who was wishing and hoping for better gas prices this year should probably skip the the U.S. Energy Information Agency’s recent 2020 Short Term Energy Outlook (STEO). Because if you’re looking for good news on prices, it’s a somewhat depressing read.

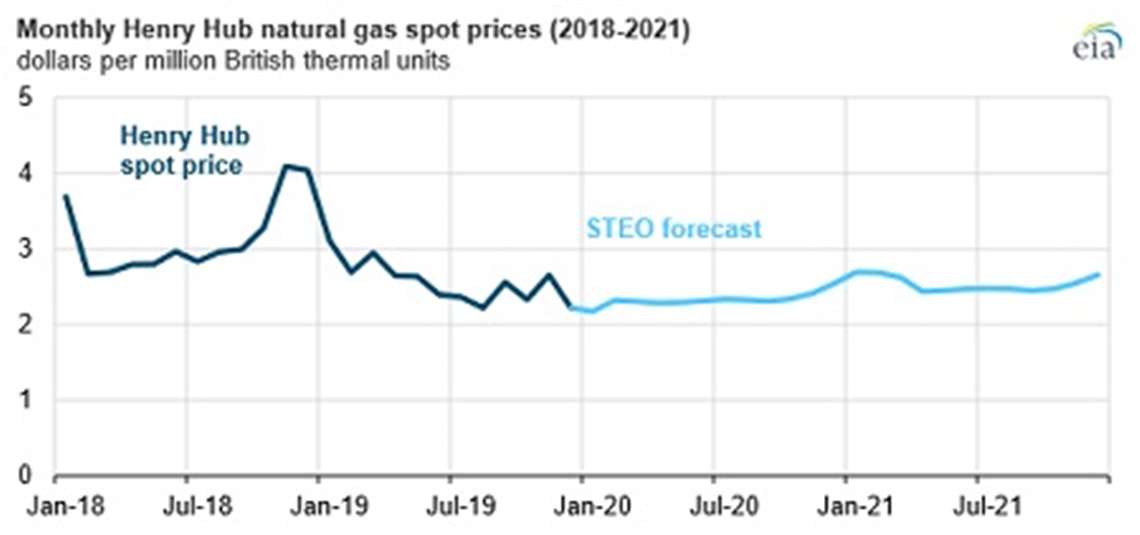

The STEO forecasts that average U.S. natural gas prices will be 9% lower in 2020 than in 2019. The agency expects lower natural gas prices will be the result of continued production growth primarily in response to:

-Improved drilling efficiency and cost reductions.

-Higher associated gas production from oil-directed rigs.

-Increased takeaway pipeline capacity from the Appalachian and Permian regions.

All of the production growth will outpace the growth in domestic demand and exports, with a negative impact on pricing, EIA said.

The agency said it expects the natural gas spot price for the U.S. benchmark Henry Hub will average $2.33 per MMBtu in 2020, about 24 cents lower than the 2019 average of $2.57/MMBtu.

But there is better news on the horizon. Following the year of decline in 2020, EIA expects 2021 natural gas prices to rise by 9% because of upward pricing pressure from declining growth in natural gas production.

EIA expects record volumes of U.S. dry natural gas production to continue through 2020, from an estimated 92.0 bcfd in 2019 to 94.7 bcfd in 2020. Most U.S. production will come from the Appalachian Basin in the Northeast, followed by the Permian Basin in western Texas and New Mexico and the Haynesville shale formation in eastern Texas. Cost reductions in drilling and well completions and improved drilling efficiency will support continued record-production levels in 2020.

In addition, a growing share of natural gas production is coming as associated gas from oil wells. Increased takeaway capacity from the highly productive Appalachian and Permian production regions will further enable growth.

However, in 2021 EIA expects dry natural gas production to decline by less than 1% to 94.1 bcfd in response to lower forecast natural gas spot prices in 2020, which would reduce Appalachian Basin production.

However, in 2021 EIA expects dry natural gas production to decline by less than 1% to 94.1 bcfd in response to lower forecast natural gas spot prices in 2020, which would reduce Appalachian Basin production.

Total U.S. natural gas consumption remains relatively unchanged compared with 2019 levels in the STEO forecast, increasing 1.7% in 2020, but decreasing 1.2% in 2021 to an average 85.7 bcfd in 2021. EIA forecasts natural gas consumption to decrease slightly in the residential and commercial sectors as a result of expected milder weather that will require less energy for space heating in the winter and air conditioning in the summer.

Based on forecasts by the National Oceanic and Atmospheric Administration, EIA forecasts 1.8% fewer heating degree days (HDD) in 2020 compared with 2019, which had a colder-than-normal first quarter.

EIA expects U.S. natural gas use in the electric power sector to increase 1.3% in 2020 as a result of natural gas-fired generation additions that continue to displace coal-fired generation. However, in 2021, because of a forecast of higher natural gas spot prices and increased competition from renewables, EIA estimates that natural gas consumption in the electric power sector will decline 3.2% in 2021. EIA expects the natural gas share of electricity generation in 2021 to be 37%, about the same as its 2019 share, while coal’s share of electricity generation will fall from 24% in 2019 to 21% in 2021.

Natural gas consumption in the U.S. industrial sector will continue to grow in 2020, increasing 4.6%. New methanol plants that use natural gas as feedstock are scheduled to come online in 2020, which will support the increased industrial sector consumption. In 2021, EIA expects industrial sector consumption to flatten because of higher industrial sector natural gas prices.

The United States became a net exporter of natural gas on an annual basis for the first time in 2018 and EIA expects that trend will continue during the forecast period. In 2020, net exports will average 7.3 bcfd — an increase of 2.0 bcfd over the 2019 levels. EIA expects 2021 net exports to rise further to 8.9 bcfd as new liquefied natural gas (LNG) projects enter service. The remaining trains at the Cameron LNG and Freeport LNG facilities, located along the Gulf Coast, and the Elba Island LNG facility in Georgia will be placed into service in 2020. EIA expects LNG exports to increase from an estimated 5.0 bcfd in 2019 to 6.5 bcfd in 2020 and up to 7.7 bcfd in 2021, more than double the 2018 level.

The United States became a net exporter of natural gas on an annual basis for the first time in 2018 and EIA expects that trend will continue during the forecast period. In 2020, net exports will average 7.3 bcfd — an increase of 2.0 bcfd over the 2019 levels. EIA expects 2021 net exports to rise further to 8.9 bcfd as new liquefied natural gas (LNG) projects enter service. The remaining trains at the Cameron LNG and Freeport LNG facilities, located along the Gulf Coast, and the Elba Island LNG facility in Georgia will be placed into service in 2020. EIA expects LNG exports to increase from an estimated 5.0 bcfd in 2019 to 6.5 bcfd in 2020 and up to 7.7 bcfd in 2021, more than double the 2018 level.

EIA forecasts that gross exports of natural gas by pipeline will continue to grow, increasing to 8.1 bcfd in 2020 and 8.5 bcfd in 2021, or 8.8% higher than the 2019 level. Most of the increase will be driven by increasing natural gas demand and by pipeline projects in Mexico that are scheduled to come online by the end of 2021. EIA expects imports of LNG to remain flat through 2021, and imports by pipeline will continue to decrease through 2020, when Appalachian production and takeaway capacity displaces imported natural gas from Canada in the U.S. Midwest markets.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM