EIA: Natural Gas To Dominate Energy Production In U.S.

24 January 2019

Natural gas will dominate new energy production in the U.S. over the next 30 years, according to the U.S. Energy Information Association (EIA)’s Annual Energy Outlook 2019, which provides modeled projections of domestic energy markets through 2050.

The report includes cases with different assumptions about macroeconomic growth, world oil prices and technological progress. But the report’s reference case—which outlines what is seen as most likely to happen—shows natural gas consumption for electric power also increases significantly in the power sector in response to low natural gas prices and to installing lower cost natural gas-fired combined-cycle generating units.

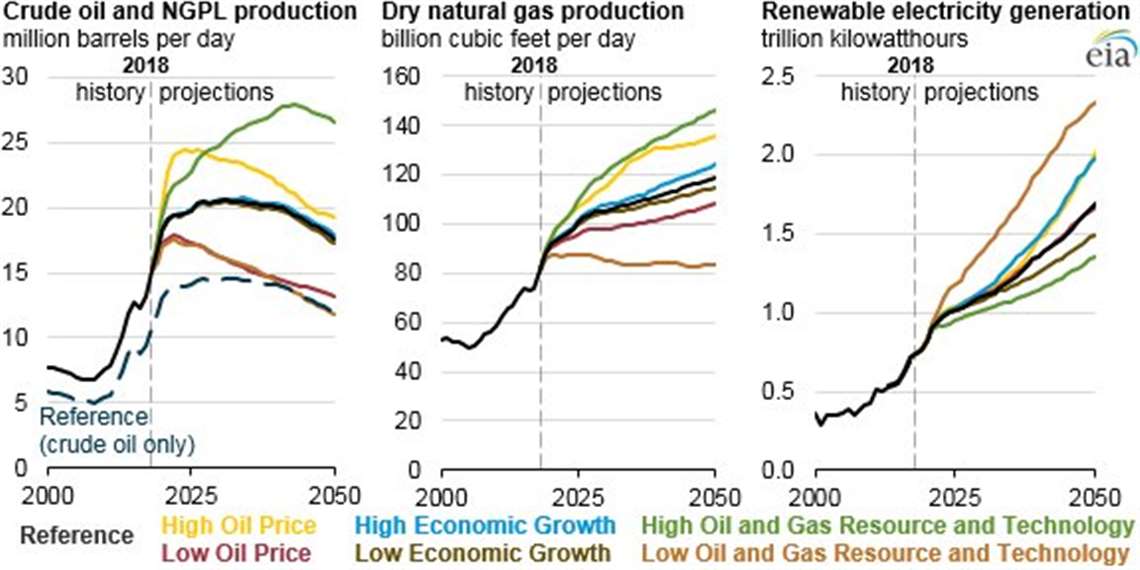

In the reference case, U.S. natural gas trade, which includes shipments by pipeline from and to Canada and to Mexico as well as exports of liquefied natural gas (LNG), will be increasingly dominated by LNG exports to more distant destinations. The continued development of tight oil and shale gas resources supports growth in natural gas plant liquids (NGPL) production, which reaches 6.0 million b/d by 2029 in the Reference case.

The percentage of dry natural gas production from oil formations increased from 8% in 2013 to 17% in 2018 and remains near this percentage through 2050 in the reference case. According to the EIA, growth in drilling in the Southwest region, particularly in the Wolfcamp formation in the Permian basin, is the main driver for natural gas production growth from tight oil formations.

The Low Oil Price case, with the U.S. crude oil benchmark West Texas Intermediate (WTI, Cushing, Oklahoma) price at US$58 per barrel or lower, is the only case in which natural gas production from oil formations is lower in 2050 than at current levels.

Natural gas production in the reference case grows 7% per year from 2018 to 2020, which is more than the 4% per year average growth rate from 2005 to 2015.

However, after 2020, growth slows to less than 1% per year as growth in both domestic consumption and demand for U.S. natural gas exports slows. Natural gas prices will likely remain lower than US$4 per million British thermal units (Btu) through 2035 and lower than US$5 per million Btu through 2050 because of an increase in lower-cost resources, primarily in tight oil plays in the Permian Basin, which allows higher production levels at lower prices during the projection period.

The level of drilling in oil formations primarily depends on crude oil prices rather than natural gas prices. Increased natural gas production from oil-directed drilling puts downward pressure on natural gas prices throughout the projection period.

The report also asserts that the United States will become a net energy exporter in 2020 and will remain so throughout the projection period as a result of large increases in crude oil, natural gas, and natural gas plant liquids (NGPL) production coupled with slow growth in U.S. energy consumption.

Of the fossil fuels, natural gas and NGPLs have the highest production growth, and NGPLs account for almost one-third of cumulative U.S. liquids production during the projection period. Natural gas prices remain comparatively low based on historical prices during the projection period, leading to increased use of this fuel across end-use sectors and increased liquefied natural gas exports. Increasing energy efficiency across end-use sectors keeps U.S. energy consumption relatively flat, even as the U.S. economy continues to expand.

The continuing decline in natural gas prices and increasing penetration of renewable electricity generation have resulted in lower wholesale electricity prices, changes in utilization rates, and operating losses for a large number of baseload coal and nuclear generators.

Generation from both coal and nuclear is expected to decline in all cases. In the Reference case, from a 28% share in 2018, coal generation drops to 17% of total generation by 2050. Nuclear generation declines from a 19% share of total generation in 2018 to 12% by 2050. The share of natural gas generation rises from 34% in 2018 to 39% in 2050, and the share of renewable generation increases from 18% to 31%.

Assumptions of declining costs and improving performance make wind and solar increasingly competitive compared with other renewable resources in the Reference case. Most of the wind generation increase occurs in the near term, when new projects enter service ahead of the expiration of key federal production tax credits.

Solar Investment Tax Credits (ITC) phase down after 2024, but solar generation growth continues because the costs for solar continue to fall faster than for other sources.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM